In some cases, you can withdraw money from your Individual Savings Account (ISA) without losing any tax benefits. However, it’s important to check the terms of your ISA account to see if there are any rules or charges for making withdrawals.

Before withdrawing money from your ISA, it’s also important to note that you stop earning tax-free interest on the amount you take out – unless you have a flexible ISA. You have a tax-free annual ISA allowance of £20,000 every tax year. This limit will remain the same until at least 2030, which the Chancellor clarified in the Autumn Budget.

This means that unless you have a flexible ISA, withdrawing your money from an ISA won’t help you maximise potential returns and make the most of the tax-saving advantages.

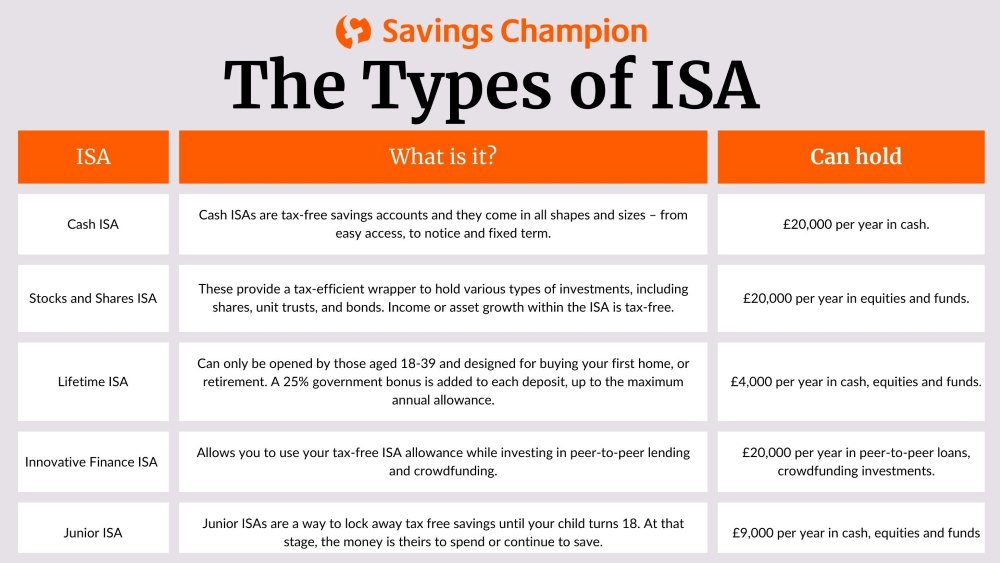

(Image Source: Savings Champion)

This article will explore the rules and charges for making withdrawals from different types of ISA accounts.

Flexible ISAs

Once you have invested money into your ISA, it counts towards your annual allowance. For example, if you had put £15,000 into your ISA this tax year but later decided to withdraw £10,000, your balance would be reduced to £5,000, but you would still have used £15,000 worth of your annual allowance.

However, if your ISA is flexible, you can withdraw money and put it back in during the same tax year without reducing your current annual allowance.

For example, if you had put £15,000 into your ISA this tax year but later decided to withdraw £5,000, you could still invest another £10,000 that tax year.

Your provider will be able to tell you if your ISA is flexible, but this is not something that is offered as standard across most providers.

Fixed Term ISAs

If you have a fixed-term Cash ISA or fixed-term Stocks and Shares ISA, you can still withdraw money before the term ends. However, you will likely be subject to an early withdrawal charge, and you may have to wait for a notice period to receive your funds.

The charges for withdrawing from a fixed-term ISA vary depending on your provider and how early you want to withdraw. For example, if you withdraw from a two-year fixed-term ISA early, you may be subject to paying 180 days of interest. If you withdraw from a three-year fixed-term ISA, you could be subject to 270 days of interest.

Your ISA provider will have specified the early withdrawal charges in your agreement, so ensure you take a look at this.

Lifetime ISAs

A Lifetime ISA is different from Cash ISAs, Stocks and Shares ISAs, and Innovative Finance ISAs, which can all be opened as flexible or fixed-term ISAs.

You cannot take money out of a Lifetime ISA without being subject to any fees unless you are using the money to buy your first house (up to the value of £450,000), you have turned 60, or you are terminally ill and have less than 12 months to live.

Unauthorised withdrawals or transfers to another type of ISA are subject to a 25% charge. This takes away the government bonus you received on your savings.

Junior ISAs

Parents or legal guardians are responsible for opening a Junior ISA, but the money belongs to the child, and they can withdraw from it when they turn 18.

The parent or legal guardian can withdraw from the account in exceptional circumstances, including:

- In the event of your child’s death: Proof of the death, such as an original death certificate or the Coroner’s interim document, must be obtained before the Junior ISA can be closed.

- If your child becomes terminally ill: You must make a terminal illness claim, which needs to be accepted before the registered contact can withdraw the funds.

- If the balance becomes £0: This can happen if a Junior ISA has been opened with a small initial investment, but contributions stop and charges bring the balance down to £0.

It’s important to note that Junior ISAs cannot be opened as flexible ISAs, as some adult ISAs can.

Do You Know Your Limits?

If you are considering withdrawing money from your ISA because you want to reinvest it elsewhere – whether into the same kind of ISA with another provider or a different ISA type – you can do an ISA transfer, which allows capital to retain its tax-free status.

Before withdrawing any money from your ISA account, read the terms and conditions that you agreed upon when you opened an account with your provider. Every provider is different.

David Prior

David Prior is the editor of Today News, responsible for the overall editorial strategy. He is an NCTJ-qualified journalist with over 20 years’ experience, and is also editor of the award-winning hyperlocal news title Altrincham Today. His LinkedIn profile is here.